Domestic India

March 31, 2025

Over the past couple of years global markets have been driven by seven mega cap technology stocks out of the US. Equity markets are broadening and the reliance on the companies is weakening, however in this note we explore an area of the market which has kept pace with the US stock market with structural tailwinds and a differentiated returns profile – India, and more specifically the companies within, who are benefiting from rapid domestic growth.

Thesis for Investing in Domestic India

Tax and banking reform have been key in helping support growth in India.

- New tax laws have sought to protect the economy from the adverse effect of cascading taxes or double taxation.

- The introduction of Aadhaar in 2009, the world’s largest biometric ID system, has lowered the barriers of entry for much of the population in opening a bank account, as it acts a valid ID in order to set up an account. Increasing financial inclusion across India will create greater opportunities for both financial returns as well as enabling positive social change.

- The introduction and implementation of the Companies Act in 2013, alongside the Insolvency and Bankruptcy code in 2016, served to reform India’s approach to corporate governance entirely.

- Looking ahead, steps are now being taken to tackle the nation’s ongoing problem of over-bureaucratisation with Indian Prime Minister Modi committing to replace a “culture of red tape” with a “red carpet”.

Changing demographics have and will continue to play a part in the Indian growth story.

- India, with the largest population in the world, also features favourable demographics with a vibrant and young population, whose average age is just shy of 30. These demographics imply the ratio of the working age population is yet to peak, quite unlike several large economies and other comparable emerging market economies.

- India’s demographics are entering a phase where the middle age (30-60) cohort is growing faster than the rest of the population. According to research conducted by Jefferies Equity Research in 2024, India will add 152 million to its middle age population who can drive savings and investment meaningfully, as those in middle age are the ones with higher discretionary income. For the next couple of decades India will enjoy the best demographics of a larger and more productive workforce, propelling economic growth with high discretionary expenditure as well as investment.

- The wealth of the general population is also growing. The number of higher income Indian households is expected to rise from 75 million to 190 million between 2021 and 2031, and households in the top in the Top 2 income brackets are also expected to grow 5.0x and 2.4x over the next decade. This rise in wealth is largely derived from the way in which Indian households distribute their wealth, making significant allocations to property, gold and increasingly, equity investments. These asset classes have experienced sustained periods of outperformance. Indian households are in real terms more well off, but also feel richer thanks to the value of their assets increasing with income and fixed costs remaining largely unchanged. This is the wealth effect in action. Increasing consumption with growing affluence.

The February 2025 Budget

The February budget brought with it perhaps one of the most significant tax cuts announced globally in recent years. The Indian government announced a tax cut for anyone earning up to INR1.2m (or $14,000) which will forego revenue of INR1trn ($11.5bn). This effectively removes approximately 75% of all taxpayers, however, it specifically benefits those citizens earning between INR0.7m and INR2.4mn ($8,000 and $28,000).

The middle class, circa 300 million strong, have already increased their discretionary spending and this latest policy will accelerate the trend. These are the types of purchases people will make when they have freely available excess capital. Spending on travel, tourism, luxury retail and cosmetics will likely rise over the next few years. Having exposure to these areas could prove to be an excellent investment opportunity whilst the wealth effect takes place. We can already see impact of wealth effect on spending within the last year. Heineken’s India arm, United Breweries, reported a five-fold increase in net profits. Godrej Properties delivered the highest ever quarterly sales for a listed real estate developer and Indian airline IndiGo’s net profits have leapt 111%, being driven by soaring domestic passenger numbers.

Another great example is Westlife Foodworld which plays into this theme as with the excess capital comes a rise in demand for convenience food. Westlife manages McDonald’s franchises in South and West India, owning over 400 outlets with the projection of opening 230 more by 2027, and has seen its share price rise by over 50% in the past 5 years as Indians have available to them that extra capital to spend on a fast-food treat.

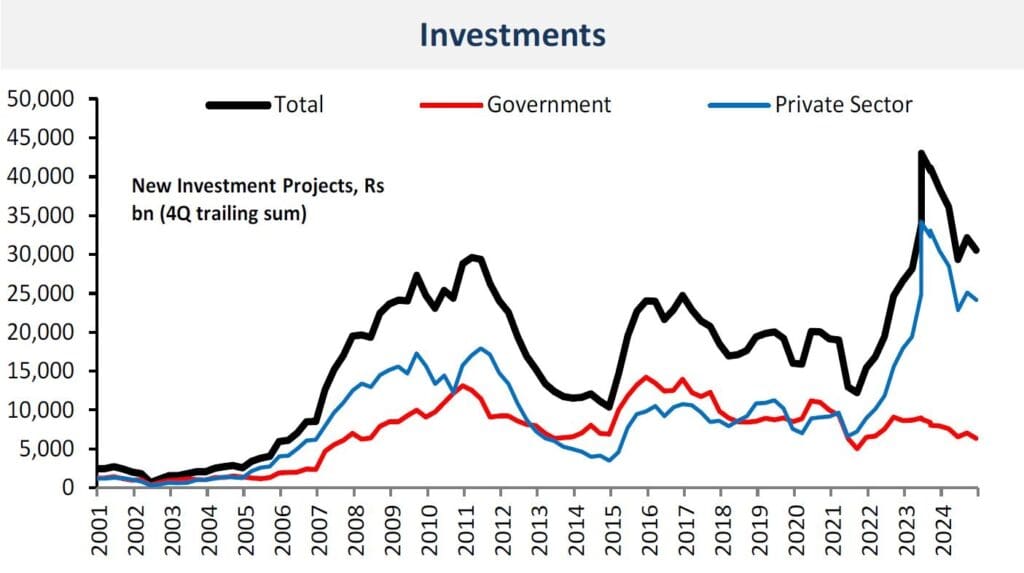

It is worth noting we believe that the clear loser in this fiscal event is capital heavy industries dependent on government infrastructure spending, where share prices and valuations have become extremely stretched.

How Quartet Invests On Behalf Of Clients

India’s exponential growth has surged out of an environment marked by heightened political and economic stability. This, coupled alongside a young workforce, an increasingly wealthy middle class and strong domestic consumption has led to the nation becoming an investment powerhouse. The fundamental structural reform has created the framework for the country to realise its full potential in terms of taking advantage of its intellectual and physical capital as well as its positive demographics.

Whilst the general performance of Indian equities in both 2023 and 2024 has been impressive, outperforming its emerging markets counterparts, Quartet wanted to focus exposure on companies who stood solely to gain from the extraordinary growth of the domestic market through a burgeoning middle class. We found this exposure in an actively managed fund. The investment process begins with a unique screening criterion: companies that export outside of India or those not expected to benefit from the themes associated with the rise of the middle class are immediately excluded. By focusing on this subset, the fund gains exposure to businesses that are often underrepresented in traditional Indian equity benchmarks.

We like the uncorrelated nature of returns and continue to hold exposure where possible on behalf of clients. When global markets are dominated by White House press conferences and geopolitical turmoil finding areas which can be insulated from such volatility is key in diversifying portfolios.

Risk Warning

This document has been issued by Quartet Capital Partners LLP (“Quartet”), which is authorised and regulated by the Financial Conduct Authority. The information in this document does not constitute, or form part of, any offer to sell or issue, or any offer to purchase or subscribe for shares, nor shall this document or any part of it or the fact of its distribution form the basis of or be relied on in connection with any contract. Quartet has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and no assurance can be given that the stated investment objectives will be achieved. Quartet may, to the extent permitted by law, act upon or use the information or opinions presented herein, or the research or analysis on which it is based, before the material is published. Past performance is not a guide to future performance.

The law may restrict distribution of this document in certain jurisdictions; therefore, persons into whose possession this document comes should inform themselves about and observe any such restrictions. This letter, the information contained herein, and any oral or other written information disclosed or provided is strictly confidential and may not be reproduced or redistributed, in whole or in part, nor may its contents be disclosed to any other person under any circumstances.

Quartet Capital Partners LLP is a Limited Liability Partnership registered in England and Wales, Company No: OC345770.

Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ.

Authorised and regulated by the Financial Conduct Authority of the United Kingdom (“FCA”).

A list of members is available for inspection at the registered office.

More insights

The Road to Victory

March 27, 2026