Five Talking Points for 2026

January 13, 2026

Welcome to 2026!

It is easy to make money when everything goes up. It is much more difficult to protect our clients’ capital when financial markets do not cooperate. In effect, we are paid to worry; we are paid to handle risk well.

What could go wrong in 2026? A great deal of time has been spent on this topic in December, when most of our clients had other things to think about. As we look at the world in front of us, three risks currently stand out. We will present them in no particular order; i.e. don’t assume we worry more about #1 than #2 or #3.

#1: US monetary policy. Our concern is that Trump will replace Jerome Powell with somebody who is prepared to lower the policy rate purely for political reasons, and that this will lead to a significant steepening of the US yield curve and, even worse, to a new spike in inflation.

Jerome Powell’s second term as the Chair of the Federal Reserve Bank ends on 23rd May this year unless he is either reappointed or walks away prematurely. We assign a very low probability to any of those outcomes; i.e., in all likelihood, a new Fed Chair will almost certainly take over in May.

Now, what does that mean? After the December rate cut, the Fed Funds target range is 3.50-3.75% with the Effective Fed Funds Rate (EFFR) being 3.64%. Trump has repeatedly said that the Fed should instantly lower the Fed Funds rate by a full percentage point and follow up with several more cuts.

Trump’s wording suggests that he wants the EFFR to be cut by at least another 1.25% in addition to the 0.25% delivered in December, and that is why we expect Powell to be replaced by somebody who is prepared to dance to Trump’s tunes. More recently, Trump has even stated that he won’t bring in a new Chair who isn’t willing to take the EFFR down by at least 1%!

If you wonder what drives Trump, it is probably fair to say that the US government is drowning in debt, and lower interest expenses would make it easier for him to deliver on his election promises. In that respect, Trump is faced with at least two challenges, though. First and foremost, the Chair is only one of 12 voting members on the Federal Open Market Committee, responsible for setting interest rates and controlling the nation’s money supply. Even if Trump can count on the support of a couple of other voting members (and he can), there is still a long way to a majority.

Secondly, Trump doesn’t control the yield curve, and bond investors could quite possibly react with much hostility to rate cuts that are not necessary. The average maturity of all outstanding US government debt is about six years. Should the yield curve steepen significantly in response to massive rate cuts, the whole exercise could actually end up being counterproductive.

#2: The AI bubble. Our concern is that the AI bubble will finally burst, and that the selloff will turn out to be far more widespread than anticipated (similar to the dotcom bust in 2000).

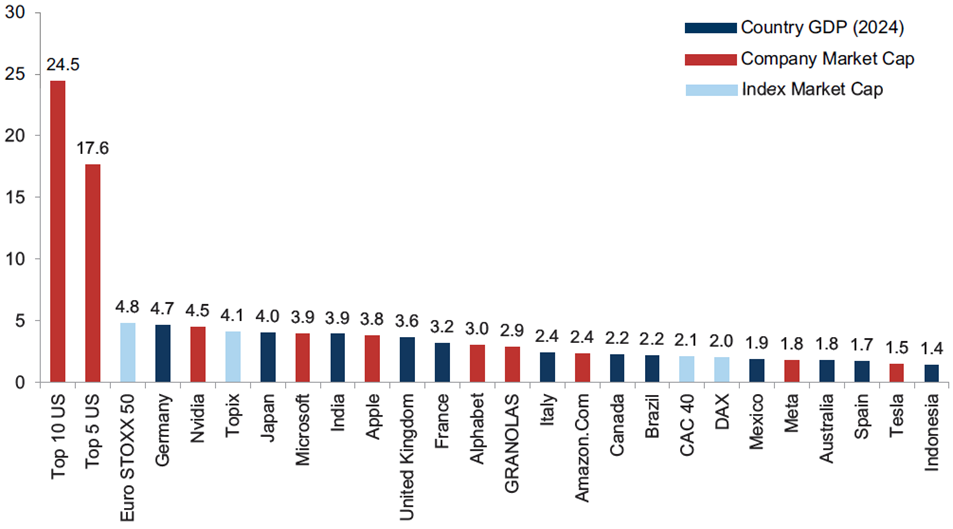

As you can see in Exhibit 1, the combined value of the ten largest US stocks, when measured by market capitalisation, now exceeds the GDP of Germany, Japan, India, UK, France, Italy and Canada put together! The ‘sinners’ here are, not surprisingly, US mega cap stocks, mostly the hyperscalers, but the rally in those has had a noticeable effect on other US equities as well.

Exhibit 1: Company market cap (red) & country GDP (dark blue) in US$ trillion

Notes: Country GDPs as of 2024. Market prices as of 8 October 2025.

Source: Goldman Sachs Global Investment Research

Even ex. Big Tech, US equities are now much more expensive than equities elsewhere. Adding to that worry, even if equites are less expensive elsewhere, with only a couple of exemptions (UK and China), equities in most countries are now trading near historical highs. This suggests to us that, if an AI-related selloff in the US were to materialise, equities in the rest of the world won’t offer the protection many expect them to. Equities elsewhere may fall less than US equities, but they will most likely still fall.

Supporters of the AI bull story argue that, yes, those stocks are indeed rather expensive, but an outstanding earnings outlook justifies it. Our counterargument has to do with the speculative behaviour of many investors in 2025. As it happens, the best performing stocks last year were Nasdaq-listed companies with no revenues, followed by unprofitable Nasdaq-listed companies!

#3: Climate change. Our concern is that our political leaders will take (even more) control of the political agenda on climate change, and that this will lead to a mix of irrational government policies.

Climate change sceptics will argue that our political leaders have already taken control and have done immense damage to the economy in the process. Our concern is that the damage has hardly started yet; things can in fact get a lot worse. Here is an example: In a recent interview with Danmarks Radio (the Danish BBC-lookalike), a Danish politician uttered the following words (and we paraphrase): “Danish households pay far too much for their electricity. We need to generate more cheap energy from wind and solar.”

If it was only that simple, but wind and solar are two energy forms that are broadly misunderstood. They are not cheap at all; they are in fact amongst the most expensive energy forms available today. On top of that, they are unreliable, as the wind doesn’t always blow, and the sun doesn’t always shine.

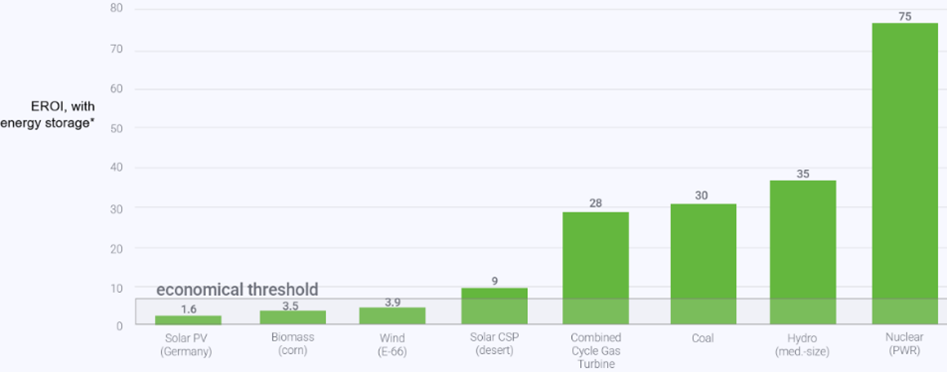

EROI (Energy Return On Investment) is a great measure of energy efficiency; hence why it is important that our political leaders understand it (but many of them don’t). It measures how much energy you get out from an energy source compared to the energy spent extracting, processing and delivering it. An EROI of 8:1 means that you generate eight units of energy for every one unit of energy invested, and 8:1 happens to be the breakeven point; the point where the energy source in question begins to make economic sense.

Exhibit 2 below compares the lifetime electricity output of different energy sources to the energy needed to create and run them 24/7, which is precisely how EROI is defined. Take a long look at the chart, and then ask yourself the question: Are our political leaders on the right track?

Exhibit 2: EROI of various energy sources

Source: enCore Energy

The bottom line for client portfolios

As we enter 2026, we think the risks facing equity investors are above average but not (yet) at extreme levels. The last major, global panic attack happened in early 2020, when it dawned on investors how serious COVID-19 was. Back in 2008, as the Global Financial Crisis unfolded, there was even more blood in the streets. Equities always react negatively to such incidents but sometimes more so than others. They are particularly sensitive when equity valuations are rich, and equities – particularly US equities – are indeed richly valued at present.

Looking into 2026, we believe three trends will govern, and will continue to dominate, our portfolio construction:

- index-linked bonds to outperform nominal bonds;

- commodities to outperform equities; and

- Rest of the World equities to outperform US equities

#1 is the consequence of the first concern referred to above, i.e. that President Trump may replace Jerome Powell with an uber-dove, which could have an unpleasant impact on inflation.

#2 is a function of the near-global focus on climate change (ex. USA). As the average temperature continues to rise, so will (most) governments’ desire to go green, and that will raise demand for many commodities, particularly green metals.

Finally, #3 is a result of our second concern, i.e. that the AI bubble may burst. It is almost a given that equity markets will be affected worldwide, should the bubble burst in the US, but we think the negative impact will be biggest in the US, given how expensive US equities are at present.

Risk Warning

This document has been issued by Quartet Capital Partners LLP (“Quartet”), which is authorised and regulated by the Financial Conduct Authority. The information in this document does not constitute, or form part of, any offer to sell or issue, or any offer to purchase or subscribe for shares, nor shall this document or any part of it or the fact of its distribution form the basis of or be relied on in connection with any contract. Quartet has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and no assurance can be given that the stated investment objectives will be achieved. Quartet may, to the extent permitted by law, act upon or use the information or opinions presented herein, or the research or analysis on which it is based, before the material is published. Past performance is not a guide to future performance.

The law may restrict distribution of this document in certain jurisdictions; therefore, persons into whose possession this document comes should inform themselves about and observe any such restrictions. This letter, the information contained herein, and any oral or other written information disclosed or provided is strictly confidential and may not be reproduced or redistributed, in whole or in part, nor may its contents be disclosed to any other person under any circumstances.

Quartet Capital Partners LLP is a Limited Liability Partnership registered in England and Wales, Company No: OC345770.

Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ.

Authorised and regulated by the Financial Conduct Authority of the United Kingdom (“FCA”).

A list of members is available for inspection at the registered office.

More insights

The Road to Victory

March 27, 2026