Gold

September 19, 2025

The price of gold has reached a record high in recent weeks, fuelled by uncertainty over the future direction of inflation and a tormented bond market, a flammable geopolitical environment, and a weakening US dollar.

We therefore thought it timely to reflect on why we hold gold in clients’ portfolios and provide an outlook given that some may question why we remain invested given the record high price.

Why Quartet holds Gold

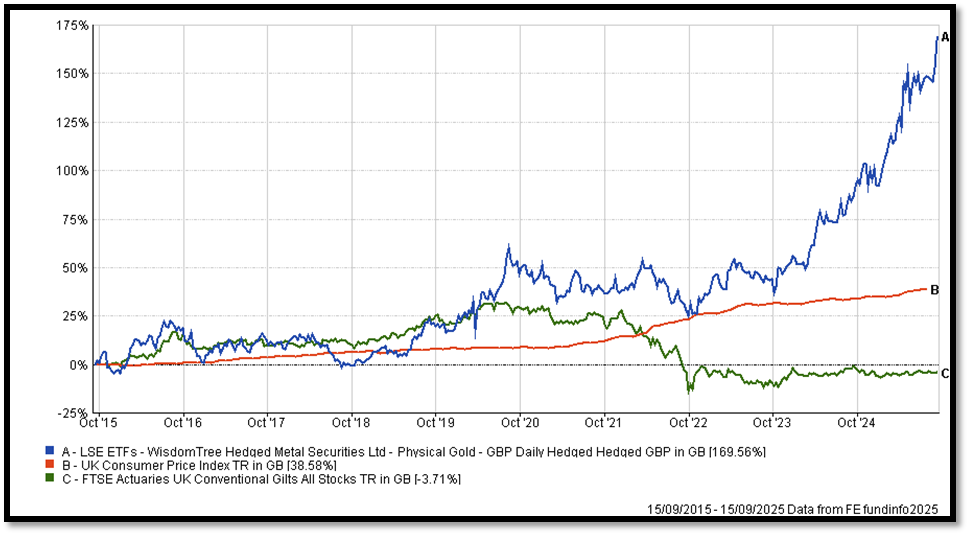

- Gold acts both as a risk management tool in portfolios and a source of expected return for clients. It has displayed low to negative correlations with bonds and equities over time, particularly when it matters. Offsetting correlations between the asset classes within portfolios dampens the levels of portfolio risk, or volatility. This helps to optimise risk-adjusted performance, especially during periods of market distress and high volatility when bonds (lower risk) can fall in tandem with equities (higher risk). Gold has also protected savings from the corrosive effects of inflation, the enemy of bond investors. The chart below displays just that (gold vs the UK inflation index and UK government bonds (gilts):

- Gold is a hedge against tail risk: the risk of rare, unexpected and often extreme events that can cause significant losses in a portfolio.

- De-dollarization. This is the ongoing change in the global monetary system which is fuelled by a combination of geopolitical shifts alongside concerns regarding the U.S. dollar’s hegemonic power as the global reserve currency. These concerns stem largely from Emerging Markets, and most notably, China. Gold’s unique attribute as a stable, finite physical asset underpin the current momentum toward de-dollarization and the appreciation of gold as a natural reserve currency substitute in the face of money printing to solve fiscal challenges for governments. This is most evident in heavily indebted western economies.

Supply & Demand

Supply:

Gold is getting harder to mine

- The gold in the ground is far less concentrated than it once was. In the 1950s, a tonne of rock might have yielded 12 grams of gold. Today it’s closer to 3 grams.

- Each year, more rock, more energy, more labour and more capital are needed to produce an oz. of gold.

- Of the total above-ground stock of gold, 22% is estimated to be locked in investment vaults, while 17% sits in central bank reserves. Much of the remainder is in jewellery, predominantly owned by Indian and Chinese households where gold jewellery is primarily viewed as a store of value.

Gold is not consumed – it is accumulated and stored

- Nearly all gold ever mined – about 220,000 tonnes – still exists.

- Only about 3,300 tonnes is mined annually these days.

- New production adds 1%+ to total supply every year, and that number is very stable and largely unresponsive to price fluctuations.

- Because mining is spread worldwide, local disruptions have little impact on price.

- Output is planned years in advance, and to bring a new mine into production takes decades, i.e., miners cannot take advantage of price spikes and increase production.

Demand:

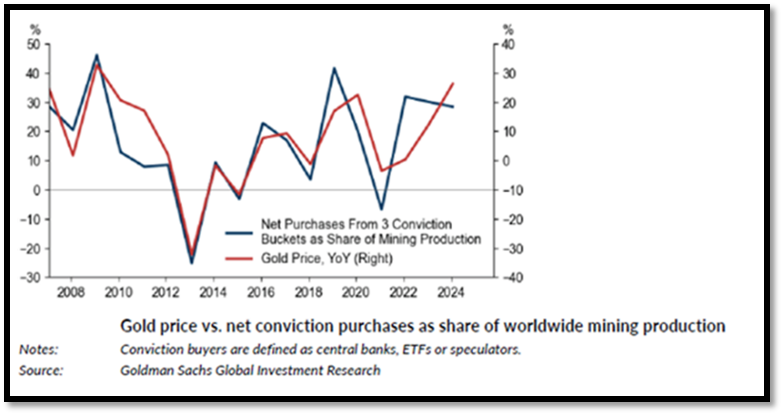

There are essentially two groups of gold buyers – conviction buyers and opportunistic buyers. The latter only step up when they feel the price is right, whereas the former allocate to gold based on their overall macroeconomic views:

- A large proportion of opportunistic buyers are passive vehicles (ETFs) and speculators such as Asian retail investors (households), whereas central banks are richly represented amongst conviction buyers.

- Opportunistic buyers provide a floor under the price on the way down and resistance on the way up.

- As a rule of thumb, 100 tonnes of net purchases by conviction buyers corresponds to a ~1.7% rise in the gold price.

- Opportunistic demand shapes amplitude, not trend. Opportunistic buying is largely irrelevant as far as trend is concerned.

- Gold price moves are essentially driven by a combination of conviction purchases and mining supply. As supply has been largely stable in recent years, changes in net conviction purchases have, more recently, accounted for nearly all price variations.

Outlook

China seems committed to its strategy to unseat the U.S. as the global economic superpower. An important part of that strategy appears to be to undermine the U.S. dollar’s position as the world’s reserve currency. A continued shift away from U.S. dollar reserves to gold reserves amongst leading Emerging Market central banks is very much part of this strategy. The fact that it is nearly impossible to meaningfully increase gold production anytime soon only adds impetus to the case for investing in gold.

Financial investors were, for a long time, absent from the gold market (based on the declining investment in gold ETFs and index funds). However, more recently, gold equities have performed better than gold bullion. Looking at the largest gold equity ETF worldwide with over $15 billion of AUM, over the last five years, it has delivered a total return to investors of approx. +51%. Over the same period, gold bullion has delivered a total return of +83%. Having said that, YTD, the return picture is noticeably different; +87% for the gold mining equity ETF vs. +51% for gold bullion.

Given the dramatic underperformance of gold equities vs. gold bullion over the last 5 years, should we at least partially replace gold bullion with gold equities?

While gold equities have outperformed physical gold year-to-date, sacrificing exposure to gold itself is not a prudent decision from our perspective. Physical gold offers crucial tail-risk protection during times of extreme market distress, an attribute that gold equities cannot fully replicate due to their tendency to correlate with the broader equity market, particularly when equities sell off.

Despite the record price of gold currently, we remain committed to maintaining a core allocation as it is a sensible way to safeguard against downside risks while still participating in the upside. Increasing wealth in India and other Emerging Markets, continued de-dollarization and robust investor demand in the face of deteriorating fiscal deficits in the West should see gold continue to increase in value in the years ahead, although periods of volatility in the price are to be expected.

Risk Warning

This document has been issued by Quartet Capital Partners LLP (“Quartet”), which is authorised and regulated by the Financial Conduct Authority. The information in this document does not constitute, or form part of, any offer to sell or issue, or any offer to purchase or subscribe for shares, nor shall this document or any part of it or the fact of its distribution form the basis of or be relied on in connection with any contract. Quartet has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and no assurance can be given that the stated investment objectives will be achieved. Quartet may, to the extent permitted by law, act upon or use the information or opinions presented herein, or the research or analysis on which it is based, before the material is published. Past performance is not a guide to future performance.

The law may restrict distribution of this document in certain jurisdictions; therefore, persons into whose possession this document comes should inform themselves about and observe any such restrictions. This letter, the information contained herein, and any oral or other written information disclosed or provided is strictly confidential and may not be reproduced or redistributed, in whole or in part, nor may its contents be disclosed to any other person under any circumstances.

Quartet Capital Partners LLP is a Limited Liability Partnership registered in England and Wales, Company No: OC345770.

Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ.

Authorised and regulated by the Financial Conduct Authority of the United Kingdom (“FCA”).

A list of members is available for inspection at the registered office.

More insights

The Road to Victory

March 27, 2026