A good six months have passed since the UK economy first went into lockdown, and a second one may now be on our doorstep. Despite the relatively high risk of this happening, equity markets in most parts of the world are behaving as if there is nothing to worry about. As you can see in Exhibit 1 below, a global equity portfolio has now largely recovered the losses from earlier this year, but we believe there is plenty to worry about so have decided to provide a brief note on this paradox.

Exhibit 1: FT All-World Index (last 5 years)

Source: markets.ft.com

Effectively, one of two things could happen going forward, neither of which justifies current equity valuations. Either equity markets are correct in projecting that economic activity will rebound relatively quickly (a V-shaped recovery), or we are in for a long and gloomy winter (a Nike Swoosh or L-Shaped recovery). If a V-shaped recovery proves correct, the excessive amount of recent money supply growth, which has been provided to stimulate a sick economy (more so by the Fed than any other central bank – see Exhibit 2), could have a rather dramatic effect on inflation as it almost always does over the long-term.

Exhibit 2: Money growth in the UK and the US

Source: Capital Economics, QMA Wadhwani

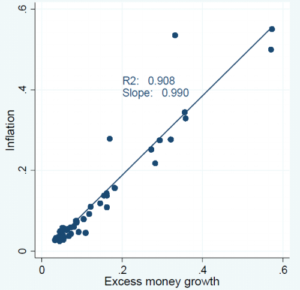

We have done some research on the recent spike in money growth as it makes us somewhat uncomfortable, and we can only reach one conclusion. As conditions gradually normalise, be it over the next one, two or three years (or even longer), money growth of the magnitude seen recently almost always causes inflation to rise significantly. We came across a research paper from Bank for International Settlements (BIS Working Paper No. 566 from May 2016) and the evidence is quite powerful. More than 90% of all long-term inflation can be explained by the growth in money supply (Exhibit 3).

Exhibit 3: Money growth and inflation

Note: Data from 46 countries from 1950 to 2011.

Source: Bank for International Settlements, Working Paper 566

As the authors of the BIS paper conclude: “This observation has reinforced calls that credit aggregates ought to be given greater attention in monetary analysis in order to better identify risks to financial stability and ultimately to long-run price stability”. In plain English, this is a stark warning – you simply cannot grow money aggregates this aggressively without serious long-term implications.

That deals with the inflation option. Now what about the alternative, recession?

If we are going into a long and gloomy economic winter (a Nike Swoosh recovery which, in our opinion, is the more likely outcome), consumer spending – a very important part of the economy – will struggle and corporate earnings will disappoint. In the UK, inflation-adjusted earnings growth has been negative in most years since the Global Financial Crisis of 2008, suppressing average living standards and GDP growth in the UK. Now, nominal earnings growth has also turned negative (Exhibit 4), and gloomy economic conditions over the next six months will do nothing to change that trend.

Exhibit 4: Average nominal earnings growth in the UK

Source: Capital Economics, QMA Wadhwani

We are dealing with the sort of economic downturn we haven’t had to deal with since the Spanish flu in 1918. Normally, in a recession, once inventory levels have been adjusted downwards, the wheels in industry can begin to spin again, but this is no normal recession. This is a recession caused by changing consumer behaviour, which again is the result of people being scared of dying or, at the very least, being afraid of passing Covid-19 to somebody who may die. Effectively, we are in the process of re-setting inventory levels in the service sector, and the only inventories of any significance there are people.

As a consequence of that, many will remain unemployed, and consumer behaviour will remain subdued, for a lengthy period of time, which is why we believe the gloomy scenario we outlined above is the more likely of the two. However, should we be overly pessimistic because, it won’t take long before ample growth in money supply begins to affect inflation and central banks be forced to reverse their very accommodating monetary policy. Neither outcome will have a positive effect on equity prices.

Conclusion

As a consequence of all of this we have increased inflation protection in portfolios via US TIPS (Treasury Inflation Protected Securities) whilst maintaining a material exposure to Infrastructure and UK Index-Linked Gilts. We also remain underweight in our long–term, or strategic, asset allocation to equity markets whilst holding higher levels of cash and Gold than normal. We have identified and continue to analyse exciting investment opportunities with low correlations to equity markets which we think should do well irrespective of market direction over the coming months.

Quartet Investment Managers – 25th September 2020