“By pulling forward consumption and pushing back failure, “ZIRP” (Zero Interest Rate Policy) and “QE” (Quantitative Easing) have warped the economic timbers. On a bad day, you can hear them creak”.

James Grant

We first presented this quote from James Grant, the eminent American writer, in our Client Letter in January 2015, and his wise words still resonate today.

It is no coincidence that the sharp fall in equities during October coincided with the U.S. Federal Reserve beginning to drain liquidity (money) from the system, following years of “QE”. Equities and bonds have prospered since 2009 due to a seemingly endless supply of cheap money provided by many central banks around the world. What goes up must come down, if the forces that drove it up go into reverse. The “normalisation” of monetary policy in the U.S. is finally underway. The same cannot be said of U.S. politics.

We do not see the current, and long awaited, correction in equity markets as cause for concern. While we understand it can be unsettling for clients to see markets fall sharply, our cautious positioning and robust risk management process mean that portfolios have been relatively well insulated from the recent sell-off. The reversal of monetary stimulus was always going to have an impact on asset prices, so we have been expecting this correction in markets for some time. As such, clients’ cash allocations have remained unusually high and provide a cushion against falling equity markets. It also means we can act quickly to buy equities when they present good value.

As monetary policy loosens its grip on asset prices, investors are having to navigate an increasingly flammable geopolitical environment which is hard to price in to markets. It is this transfer from one seemingly stable and asset-friendly monetary policy to a more unpredictable and threatening political one that we think is causing investors to re-evaluate the future. The deflationary forces of globalisation could go into reverse, should protectionism and trade tariffs become a more permanent feature of life. This will drive up bond yields, and equity valuations will have to adjust to a higher cost of capital which could cause some discomfort given the high level of indebtedness still in the system.

Then there is the economic cycle. There are many signals that suggest we are “late cycle”. Rising bond yields, a stale and lengthy bull market in equities, a strong U.S. dollar and rising wages. Rising wages are a good thing for overall purchasing power, but it means that labour is beginning to take a larger share of corporate profits, so there is ultimately less for shareholders. Equity valuations will need to reflect this.

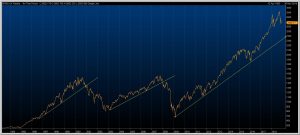

We have been underweight equities for some time (U.S. and Europe primarily) and see the current sell-off as a chance to increase exposure when and where we see value. Despite the steep declines we have witnessed in markets in recent weeks, the U.S. bull market trend remains intact (see S&P 500 chart below). Trends are powerful features of market behaviour and tend to be broken when investor momentum and confidence fade.

As far as U.S. equities are concerned, we note that officers representing the Federal Reserve have softened their tone in recent days, now openly talking about a (modest) softening of the U.S. economy in 2019. Consequently, market expectations on U.S. interest rate hikes next year may not be met.

Overall, we don’t think we have completed the sell-off yet, so patience is warranted. We do, however, see some value in UK equities which have not enjoyed the same fortunes of the U.S. equity market, so we are likely to begin increasing exposure here, despite all the Brexit noise. Our underweight positioning in emerging market equities has benefitted portfolios. We sense that much of the bad news is priced in to these markets (the fund we are monitoring is down 30% this year), and we are keen to rebuild our long-term strategic allocation in order to capture the long-term potential of returns in fast growing regions of the global economy.

S&P 500 Equity Index, 1993 – 2018

Source: ProQuote

Quartet Investment Managers