Stalemate in Iran

March 11, 2026

“Iran remains defiant and U.S. midterm elections are less than eight months away”

Those two statements probably sum up the state of affairs better than anything else. Why? Because Iran has a new leader who is determined to follow in his father’s footsteps, and because relatively cheap Iranian military technology (mostly drones) has proven effective against the Americans’ trillion dollar military extravaganza. In fact, so effective that the Americans are trying to tell a puzzled world that the military campaign is now largely complete, that there is no Iranian navy or air force left, and that the Americans can therefore pull out quite soon.

That last point brings us to the second opening statement. A recent Reuters poll showed that only one in four Americans support the war in Iran. With the House of Representatives looking likely to go to the Democrats, the Republicans can hardly afford so much resistance. Although Trump immediately labelled the Reuters poll “fake news”, it is obvious that he is rattled. In the press conference on the 9th of March, he desperately looked for reasons to chicken out (again).

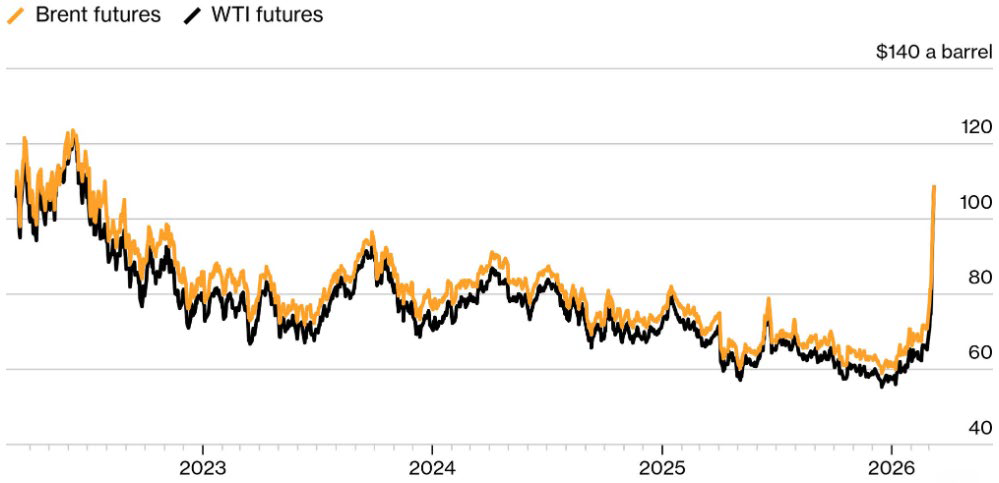

What did he really mean when he indicated that the Americans may pull out “quite soon”? In days? In weeks? Any longer? And where does that leave the Israelis? Nobody knows. When trading started on the 9th of March, Brent oil was over $100/barrel – up from about $65/barrel only ten days ago (Exhibit 1).

Exhibit 1: Oil prices since January 2023

Note: The overnight spike between 09/03/2026 and 10/03/2026 not included

Source: Bloomberg

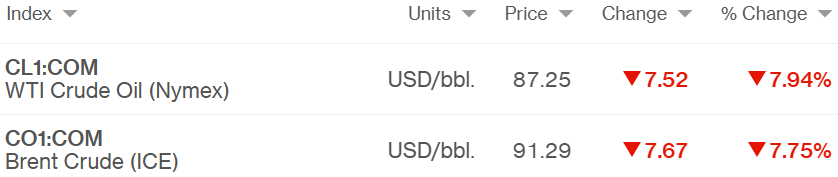

Trump then went live with various suggestions. Pulling out of Iran ”quite soon” was on the agenda, but it was far from the only suggestion. He talked about releasing strategic oil reserves, and he even mentioned the possibility of easing oil sanctions against Russia. The impact was immediate. The S&P 500, which was in red most of the day reversed and ended the day up 0.83%. Meanwhile, oil prices collapsed and are down to about $90/barrel this morning in Europe (Exhibit 2). Trump always chickens out!

Exhibit 2: Oil prices between 09/03/2026 and 10/03/2026

Source: Bloomberg

Now to the most important question: What’s next?

We believe Trump is rattled because he is no longer in full control of the Republican Party. The Democrats are not the only ones trying to unsettle him. From within his own party, the angry voices are getting louder, and the objective is obvious. Should the House go to the Democrats, the next two years will become a great deal more complicated on Capitol Hill. The aim is therefore to put a lid on the can of worms Trump opened by attacking Iran and, so far, Trump appears willing to follow that line.

Precisely how the Israelis will handle a US pull-out remains a big question. For years, they wanted to destroy Iran, and we are pretty sure (but don’t know for certain) that, if it was up to them, what you have seen so far was only the beginning. Will they continue without the Americans, though? We doubt it and therefore think energy prices will continue to normalise. However, if the US and Israel have underestimated the resilience of the Iranian regime then instability in the region is likely to continue, even after the US has left the conflict, commanding a geopolitical risk premium on oil and gas prices for some time to come.

How have we positioned portfolios given the geopolitical turmoil?

Portfolios have been positioned with an explicit focus on the resilience and stability of returns through periods of heightened volatility and uncertainty. This has meant maintaining a material allocation to gold and industrial metals as a hedge against both inflationary pressures and geopolitical risk, while also providing diversification away from traditional equity and bond markets. We increased our exposure to Invesco’s oil & gas ETF toward the end of last year. While we could not predict recent events in the Middle East, we were of the opinion that energy assets were being priced too pessimistically relative to their long‑term fundamentals, especially given the green transition and demand from AI infrastructure.

Within equities, the emphasis remains firmly on businesses with strong balance sheets, robust cash generation and proven business models, rather than more speculative companies with no profits and high levels of debt that could be particularly vulnerable in a more stagflationary environment. As a result we have maintained an underweight exposure to the US and technology in particular.

Our fixed interest exposure remains heavily focussed on inflation-linked government bonds, both UK and US, which should perform well in a stagflationary environment and also provide some degree of protection should equity markets fall. In addition, within our alternatives allocation we maintain a high exposure to infrastructure which also provides a degree of inflation linking.

Our aim is to balance participation in long‑term growth with an appropriate level of downside protection given the uncertain macroeconomic backdrop.

Risk Warning

This document has been issued by Quartet Capital Partners LLP (“Quartet”), which is authorised and regulated by the Financial Conduct Authority. The information in this document does not constitute, or form part of, any offer to sell or issue, or any offer to purchase or subscribe for shares, nor shall this document or any part of it or the fact of its distribution form the basis of or be relied on in connection with any contract. Quartet has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and no assurance can be given that the stated investment objectives will be achieved. Quartet may, to the extent permitted by law, act upon or use the information or opinions presented herein, or the research or analysis on which it is based, before the material is published. Past performance is not a guide to future performance.

The law may restrict distribution of this document in certain jurisdictions; therefore, persons into whose possession this document comes should inform themselves about and observe any such restrictions. This letter, the information contained herein, and any oral or other written information disclosed or provided is strictly confidential and may not be reproduced or redistributed, in whole or in part, nor may its contents be disclosed to any other person under any circumstances.

Quartet Capital Partners LLP is a Limited Liability Partnership registered in England and Wales, Company No: OC345770.

Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ.

Authorised and regulated by the Financial Conduct Authority of the United Kingdom (“FCA”).

A list of members is available for inspection at the registered office.

More insights

The Road to Victory

March 27, 2026