The Greenspan Put Re-Visited

July 8, 2026

Do you remember the Greenspan Put? Named after Alan Greenspan, Chairman of the Federal Reserve Bank (the Fed) from 1987 to 2006, it became synonymous with “buy every dip, because Greenspan will make sure markets go up again.” The term describes the belief that the Fed, under Greenspan, would intervene to rescue stock markets during downturns.

When the market fell beyond a certain threshold, rates would be cut to inject liquidity and support equity valuations. It functioned like an insurance policy for investors, similar to a financial “put option”, effectively limiting downside risks. It is probably fair to say that the Greenspan Put was the main reason U.S. equities kept rising throughout the 1990s despite becoming increasingly overpriced.

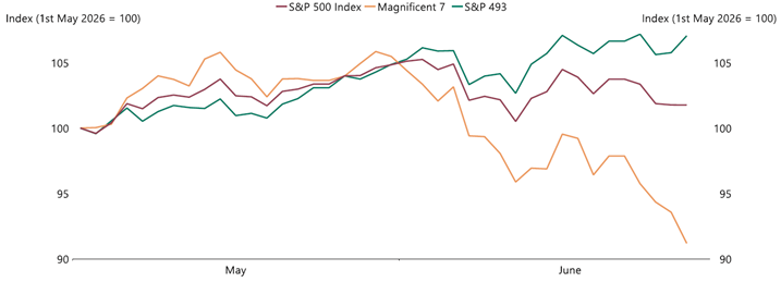

Fast forward to the 2020s, and we strongly suspect the Greenspan Put has been resurrected. It all started with the Magnificent 7, which performed extraordinarily well in 2023, 2024 and 2025. However, since mid-May of this year, fortunes have changed. As you can see in Exhibit 1 below, the Magnificent 7 have significantly underperformed the S&P 500 over the last 7 weeks and, if you exclude them from the index (aka S&P 493), the underperformance has, not unsurprisingly, been even bigger.

Exhibit 1: Magnificent 7 vs. S&P 500

Source: Apollo Global Management

This raises two important questions:

1. Has the Greenspan Put finally been put to rest?

2. If it has, why do U.S. equities keep going higher?

The two questions are essentially part of the same story, so we’ll answer them as one. No, we don’t think the Greenspan Put is dead. In fact, to the contrary. The Greenspan Put is very much alive and kicking. However, investors are increasingly concerned about the hyperscalers’ desire to outspend each other. Last year, $412 Bn was spent on capex between Alphabet, Amazon, Meta, Microsoft and Oracle. That is expected to grow to $750Bn this year and to almost $900Bn next year.

The numbers are getting so big that the free cash flow in those companies is no longer sufficient to cover all spending. Debt levels have therefore started to rise as well. That has reminded investors of the late 1990s where corporate debt also grew fast, as technology companies continued to outspend each other. Back then, as we know now, it all ended in tears. Many technology companies were bankrupted, and many of those which survived had a horrid time in the dotcom bust between 2000 and 2002. The tech-heavy Nasdaq index fell 78% (!) from the peak in March 2000 to the trough in October 2002. By comparison, the broader S&P 500 index fell ‘only’ 49%.

One of the most important lessons learnt from the dotcom bust, and one which may actually provide the answer to the second question above, is that, in the end, internet users benefitted a great deal more than those who made it all happen. Could the same happen again? We believe investors increasingly think so.

Goldman Sachs provides monthly updates on AI adoption amongst U.S. corporates. The research paper is named AI Adoption Tracker, and the latest paper from June suggests AI adoption is now, for the first time ever, higher than 20% (in June, it was 20.6% to be precise). In the paper, Goldman Sachs also provides forward-looking estimates, and AI adoption in the U.S. is expected to rise to 23.9% within the next six months. This is important, as it is a manifestation of investor beliefs that AI will have a very positive impact on the U.S. economy for many years to come.

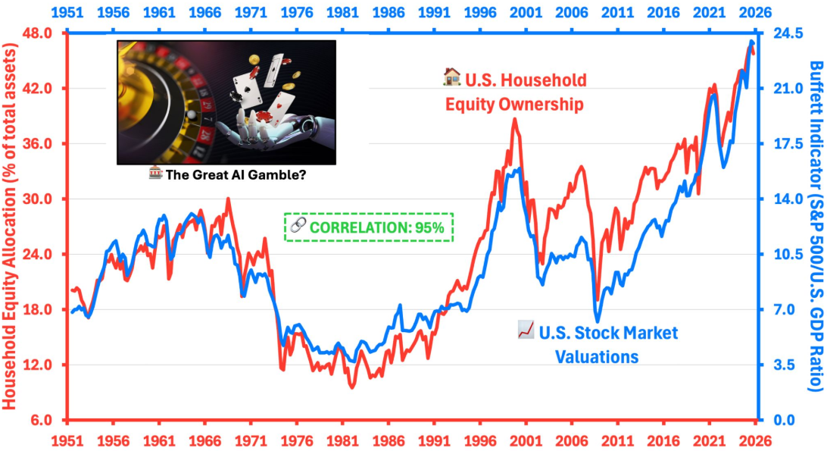

Going back to the two questions raised above, Exhibit 2 probably answers them better than anything else. As you can see, since the Global Financial Crisis in 2007-08, U.S. equities have gradually become more and more expensive. However, as you can also see, that has not led to a reduction in shareholding amongst U.S. private investors. To the contrary. As valuation multiples have risen, so has ownership. That would never have happened if the Greenspan Put had been buried. Private investors quite clearly remain convinced that the Greenspan Put is still there as a backstop.

Exhibit 2: Equity ownership in U.S. households vs. U.S. equity valuations

Source: Tom Bradshaw

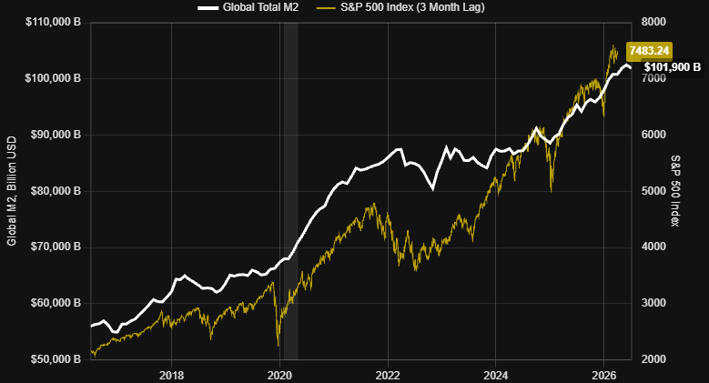

Having said all of that, the Greenspan Put is not the main reason U.S. equities took off in the first place. Ample liquidity is, we believe. Take a look at Exhibit 3, where you can see the performance of the S&P 500 in recent years vs. global liquidity (measured by global M2). As you can see, if the S&P 500 is lagged by 3 months, there is almost a 1:1 relationship between the two.

Exhibit 3: Global M2 vs. S&P 500

Note: S&P 500 lagged by 3 months

Source: State Street Management

Now to the key point of this note. We believe global M2 has started to deteriorate. If correct, it is only a question of time before the S&P 500 will head in the same direction. Crude oil prices may be back to pre-war levels, but refined oil products – most importantly petrol, diesel and jet fuel – are not. Why? Because so much refining capacity was damaged in the war, and you don’t build a new refinery in weeks. And, most importantly, higher prices on refined oil products act as a tax on consumers and thus hurt liquidity.

Just one comment to wrap it all up: Even if the Greenspan Put is still in place, when equity valuations are this rich, it always ends in tears. Over the last 125 years, we have ‘enjoyed’ three prior episodes of extreme overvaluation – New York in 1929, Tokyo in 1990 and New York in 1999. This is episode number four. The first three all ended in tears. Enough said.

Given these structural headwinds and the clear risks surrounding this episode of apparent overvaluation, a proactive and balanced approach to portfolio construction is vital. We remain close to fully invested in equity markets for clients to ensure we capture ongoing momentum, but we are watching conditions with caution and advocate for diversified assets, be that in fixed income, alternatives, or even uncorrelated equities. Relying solely on a central bank backstop during periods of such rich valuations and fading liquidity is a risk. By ensuring portfolios are anchored by assets that move independently of the overextended tech ecosystem, we aim to protect capital and smooth out the ride as these macroeconomic shifts play out.

Risk Warning

This document has been issued by Quartet Capital Partners LLP (“Quartet”), which is authorised and regulated by the Financial Conduct Authority. The information in this document does not constitute, or form part of, any offer to sell or issue, or any offer to purchase or subscribe for shares, nor shall this document or any part of it or the fact of its distribution form the basis of or be relied on in connection with any contract. Quartet has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and no assurance can be given that the stated investment objectives will be achieved. Quartet may, to the extent permitted by law, act upon or use the information or opinions presented herein, or the research or analysis on which it is based, before the material is published. Past performance is not a guide to future performance.

The law may restrict distribution of this document in certain jurisdictions; therefore, persons into whose possession this document comes should inform themselves about and observe any such restrictions. This letter, the information contained herein, and any oral or other written information disclosed or provided is strictly confidential and may not be reproduced or redistributed, in whole or in part, nor may its contents be disclosed to any other person under any circumstances.

Quartet Capital Partners LLP is a Limited Liability Partnership registered in England and Wales, Company No: OC345770.

Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ.

Authorised and regulated by the Financial Conduct Authority of the United Kingdom (“FCA”).

A list of members is available for inspection at the registered office.