The Road to Victory

March 27, 2026

There are signs of diplomatic efforts to bring the conflict in the Middle East to an end and we hope that a solution can be found. If no agreement is reached, Trump can still declare “victory” and walk away from the conflict to appease his electorate, and financial markets, before the mid-term elections in November.

In the scenario where Israel continues to fight unilaterally, after the US has withdrawn from the region, then it is likely the Gulf States will have to deploy their own military, changing the dynamics of the war with implications for energy prices beyond the perceived timeline of the conflict in its current form.

Below we set out how markets, and clients’ portfolios, are likely to react in three possible scenarios:

Scenario 1: Diplomatic Resolution

Assuming the Strait of Hormuz is fully reopened, most likely on the condition that economic sanctions imposed on Iran are lifted, then financial markets will rally although petrol, diesel, and other oil product prices may not fall as much as is hoped given how much refining capacity has been damaged during the conflict and how long it will take to rebuild. As important, is that the reopening of the Strait will remove the risk that fertilizer fails to meet the planting season this Spring, which would have huge consequences for food supply in the northern hemisphere.

Clients’ portfolios should do well in this scenario as bonds and equities should rally together as the threat of much higher inflation is removed.

Scenario 2: US “Victory” Declaration

If Trump’s version of victory means that the US and Israel have sufficiently degraded Iran’s nuclear, military and governmental infrastructure then they can walk away hoping that is enough for Israel too. However, without regime change, the risks for Israel will remain.

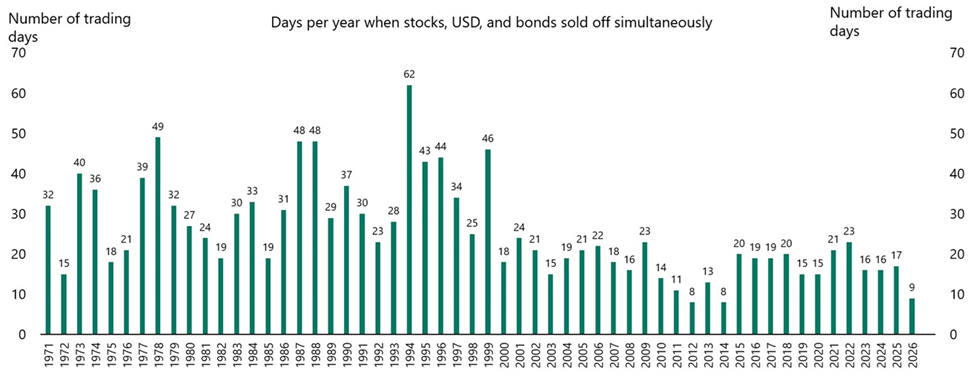

Markets will be relieved but sceptical so we would expect a relief rally in equities that is likely to be short-lived given that the Iranian regime remains in power and no security guarantees for the region are likely to have been agreed. With mid-term elections looming in November, Trump will be keen to see U.S. markets perform strongly, viewing market confidence as a key barometer of his administration’s economic success and voter sentiment. There has been talk of the “Sell America” trade, i.e. the trade in which US stocks, bonds and the dollar fall at the same time. Counting the number of days when this has happened shows no signs of 2025 and 2026 being anything special.

Exhibit 1: Days per year when stocks, USD, and bonds sold off simultaneously – as at 22nd March 2026

Source – Apollo Chief Economist

In this scenario, clients’ portfolios are likely to perform reasonably well but we may look to reduce equity exposure after an initial market rally. Inflation protection assets, like index linked bonds and infrastructure, should help to mitigate any downside risk from continued fragility in the Middle East and a persistent geopolitical risk premium on oil and gas prices.

Scenario 3: Continuation of the Conflict

This is dependent on the dominance of the hardliners within the Iranian regime and their theocratic will to degrade both Israel and the US. We think this is the least likely outcome but it would undoubtedly lead to oil reaching $150 and global food production suffering from a material shortage of fertilizer. In this scenario, portfolios are likely to suffer but do relatively well given clients’ investments in oil and gas equities, gold and inflation-linked government bonds. If we viewed this scenario playing out we would likely raise cash levels to dilute any downside in risk assets.

How have we positioned portfolios weighing up the probabilities of the above?

Currently we view Scenario 2 as the most likely outcome. A credible “Trump victory in Iran” announcement that clearly ends escalation and secures oil supply routes would likely trigger an increase in risk appetite, though the magnitude and durability of that move would depend on whether markets truly believe the conflict and associated energy risks are contained. Beneficiaries will be equities including emerging markets (excluding energy importers) where we are adding further exposure.

Potential losers in a clean de-escalation are oil, some energy equities, and safe havens like gold and long dated US government bonds. We have been taking some profits in oil and gas equity positions following year to date outperformance of roughly 40%, but we continue to hold some exposure as the upside for beneficiaries of higher oil prices remains only partly priced in. We hold no long dated US government bonds and have previously taken profits on our long standing gold position.

We are ever mindful that we are managing portfolios in a highly dynamic situation. As a result should we feel either Scenario 1 or 3 become the likely outcome we will adjust portfolios to reflect the change in risk and also opportunity set.

Risk Warning

This document has been issued by Quartet Capital Partners LLP (“Quartet”), which is authorised and regulated by the Financial Conduct Authority. The information in this document does not constitute, or form part of, any offer to sell or issue, or any offer to purchase or subscribe for shares, nor shall this document or any part of it or the fact of its distribution form the basis of or be relied on in connection with any contract. Quartet has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and no assurance can be given that the stated investment objectives will be achieved. Quartet may, to the extent permitted by law, act upon or use the information or opinions presented herein, or the research or analysis on which it is based, before the material is published. Past performance is not a guide to future performance.

The law may restrict distribution of this document in certain jurisdictions; therefore, persons into whose possession this document comes should inform themselves about and observe any such restrictions. This letter, the information contained herein, and any oral or other written information disclosed or provided is strictly confidential and may not be reproduced or redistributed, in whole or in part, nor may its contents be disclosed to any other person under any circumstances.

Quartet Capital Partners LLP is a Limited Liability Partnership registered in England and Wales, Company No: OC345770.

Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ.

Authorised and regulated by the Financial Conduct Authority of the United Kingdom (“FCA”).

A list of members is available for inspection at the registered office.