The US Election

October 3, 2024

The Election Landscape

On 21 July 2024, Joe Biden withdrew from the 2024 Presidential race and endorsed his Vice President, Kamala Harris to run for President. Many Democrats wanted an open selection process so they could assess some strong potential candidates but that was not to be. The Biden endorsement cleared the way for Harris’ path to the Democratic Party nomination.

With Biden’s withdrawal, Trump is now the “old” candidate, and his misstatements and physical mis-queues are now getting the attention Biden’s used to attract. Harris has, so far, posted few policy positions and the Republicans are trying to demonize the Democrats as far-left socialists. This is proving difficult, as Harris’ few policy positions are less left of centre than her 2020 positions. Harris has adopted Trump’s proposal to exempt service industry tips from taxable income and has promised to hire many more border guards at the Mexican border to dampen down the immigration issue. As we predicted, she is running as the moderate Attorney General she was before the 2020 campaign.

We are just over a month away from the election and the landscape is still fraught with uncertainty. In the Presidential election, though still too close to call, Harris’ marginal lead is gradually getting bigger. In the latest poll of polls, Harris leads Trump 49.3% to 46.0%. Though growing, it should be stressed this lead is still within the bounds of statistical uncertainty. However, with almost all polls now suggesting she has a slim lead, the statistical uncertainty is, in our eyes, reduced. It takes 270 electoral college votes to win the keys to the White House, and in the latest NY Times state polls, Harris stands to win 270 vs 268. In other words, it is still incredibly close.

Regarding the Senate, 34 of the 100 seats are up for election, and the outcome for those is also too close to call. That said, the most likely result as it currently stands is a either a 50-50 split or 51-49 victory in favour of the Republicans.

In the House, our view is leaning towards a Republican victory. In most states where the Republican candidate is in the lead, he/she is solidly in the lead, whereas the Democratic candidates, when in the lead, almost always holds only a marginal lead. It won’t take much for the Democrats to lose one or two seats in that race.

Overall, we believe the most likely outcome consists of Harris becoming President, with the Republicans winning both chambers of Congress. With a month to go, should Trump gain momentum, it is quite possible for there to be a clean sweep in the Republicans favour. Oil stocks will react positively to this news, and unsurprisingly, green stocks will suffer. However, if there is no clean sweep, the Inflation Reduction Act (IRA) will stand, painting a far brighter picture for green stocks. One could even argue Trump is too much of a wheeler-dealer to touch the IRA, even with a clean sweep. Many Trump supporters have landed a job because of the Act, and the former president will be reluctant to hurt this core part of his voter base.

How should investors think about the potential post-election landscape?

So far, Harris’s campaign has been light on policy details. What she has said is centre-left (by US standards) but considerably more centrist than her position in 2020. For example, she has walked-back her opposition to fracking. Trump policy highlights include higher tariffs, particularly on imports from China, lower taxes and potentially less Federal Reserve independence.

We believe that financial markets will react to the post-election situation in different ways, depending on the actual situation on the ground, which could well go beyond Bush/Gore or Biden/Trump complexity. A peaceful transition to a new President looks like the least likely scenario for now. Our bottom line is that, depending on the degree of election-related controversy, markets will either go quiet and/or defensive.

Let’s take a middle ground scenario. Lots of bluster, allegations and challenges, hyperbole and threats, but the system withstands the pressure again, and what appears to be the correct result is eventually confirmed. This still means more than two months of uncertainty from Election Day to Inauguration Day. Those ten weeks could be both volatile and tempestuous.

The US dollar will probably strengthen if it looks as if Harris will win (on the back of more public spending and, thus, higher interest rates). If the election goes Trump’s way, it will depend on how serious he is about taking power away from the Federal Reserve. Having said that, we really can’t call the final result of all the machinations and challenges until we know the outcome. To paraphrase baseball folklore, “it ain’t over till it’s over”.

The Impact of Import Tariffs on Prices and Growth

Should Donald Trump win in November, he has vowed to implement his proposed tariff programme. He has suggested several models, but Goldman Sachs have predicted the model we discuss below is the one most likely chosen. This model, the so called 10/20 model, will lead to a 20% tariff (average) on imports from China, and a 10% tariff on imports from the rest of the world. This does not imply that Kamala Harris will not do something similar. She is also pro-tariffs and will most likely also raise import tariffs, should she win. The only difference is that Kamala Harris has been very vague on her intensions so far, whereas ‘”vague” is hardly the right word to describe Donald Trump’s demeanour. Therefore, we are almost forced by circumstances to zoom in on Trump’s proposal(s), but it is important we understand that, whoever wins in November, the US is likely to significantly increase its import tariffs under the next President.

Historically it has been shown tariffs hamper economic growth and increase inflation. The higher proposed tariffs are likely to negatively affect GDP growth globally, particularly in North America. Also, an impending increase in trade policy uncertainty, similar to the 2018-2019 trade war, could result in a significant hit to investment, especially in large export-countries.

The problem the Americans are up against is that higher tariffs almost always lead to retaliation, which is effectively why the claim that higher import tariffs will lead to more jobs at home is incorrect. Retaliation is akin to trade war, as the more the Americans raise US import tariffs, the more likely it is that we end up in a nasty trade war which is bad for everybody, as it is impacts GDP growth, inflation and equity returns worldwide.

Who will be the Winners & Losers in the Financial Markets?

Assuming the 10/20 model will be implemented, Mexico should benefit the most, but many countries will see higher exports. Companies negatively affected by higher US tariffs have already started to underperform, so it may be the case higher tariffs already been discounted by the market. The US dollar is likely to suffer, with many international trades being settled in US dollars. Despite having been strong for the last 15 years, another trade war could accelerate the move towards more international trade being settled in Chinese Yuan.

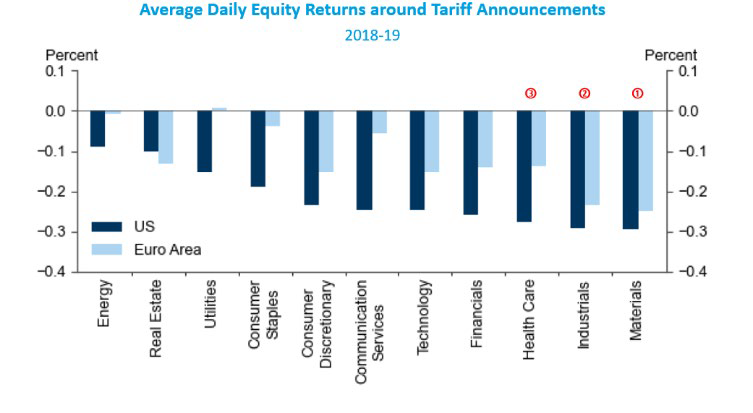

In terms of sectors, during the last trade war, industrials, materials and healthcare took the greatest hit.

Source: Goldman Sachs Global Investment Research

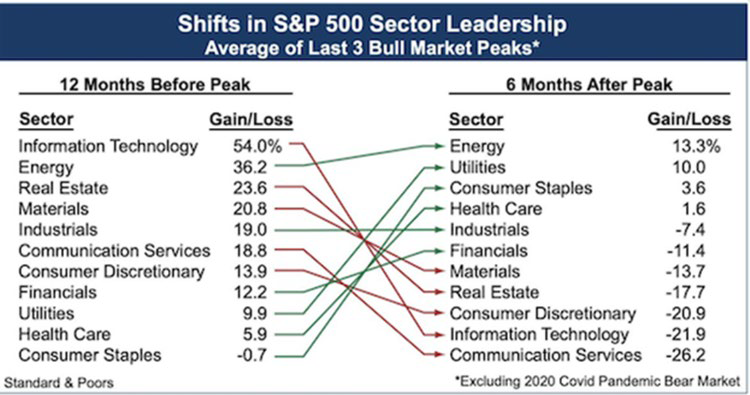

As investor sentiment shifts, the impact from sectoral rotation could be dramatic:

Source: Jesse Felder, InvesTech Research, Standard & Poors

One might wonder why the two candidates both favour higher tariffs, if both GDP growth and inflation are negatively affected. The reality is however that this is not about economics but about politics. US voters like a more aggressive stance on imported goods and services, and both Trump and Harris want to appeal to them. The retaliation argument is completely ignored.

Client Portfolios

We remain relatively agnostic about the outcome of the election as it is impossible to call. However, clients’ portfolios are well positioned to benefit from any shift in sectoral leadership within equity allocations as set out on in the table earlier, given our underweight exposure to the U.S. and within that, Information Technology. We will also take advantage of any volatility in markets between now and November with the purpose of tactically enhancing portfolio returns as value presents itself along the way.

Risk Warning

This document has been issued by Quartet Capital Partners LLP (“Quartet”), which is authorised and regulated by the Financial Conduct Authority. The information in this document does not constitute, or form part of, any offer to sell or issue, or any offer to purchase or subscribe for shares, nor shall this document or any part of it or the fact of its distribution form the basis of or be relied on in connection with any contract. Quartet has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and no assurance can be given that the stated investment objectives will be achieved. Quartet may, to the extent permitted by law, act upon or use the information or opinions presented herein, or the research or analysis on which it is based, before the material is published. Past performance is not a guide to future performance.

The law may restrict distribution of this document in certain jurisdictions; therefore, persons into whose possession this document comes should inform themselves about and observe any such restrictions. This letter, the information contained herein, and any oral or other written information disclosed or provided is strictly confidential and may not be reproduced or redistributed, in whole or in part, nor may its contents be disclosed to any other person under any circumstances.

Quartet Capital Partners LLP is a Limited Liability Partnership registered in England and Wales, Company No: OC345770.

Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ.

Authorised and regulated by the Financial Conduct Authority of the United Kingdom (“FCA”).

A list of members is available for inspection at the registered office.

More insights

The Road to Victory

March 27, 2026